Almost thirty years ago, the business scholar Clayton Christensen coined the term "The Innovator's Dilemma.”[1] His framework helps explain why even companies with a great track record tend to struggle in coping with disruptive innovations that redefine their markets.

Take incumbent utilities. Traditionally, managing electricity demand or digitizing their services has rarely been among their top priorities, nor did it need to be. Yet it is exactly these types of skills and business models that will be as essential as expanding capacity for the renewable transition to succeed. Ideally, electricity production should take place close to where and when it is needed, with demand responding to intermittent renewable production. None of this is going to be easy.[2] But the basic issues involved, including the need for electricity storage and the potential of electric vehicles and other “smart” devices to help smooth intra-day demand at the regional or even local level, has been recognized for decades.

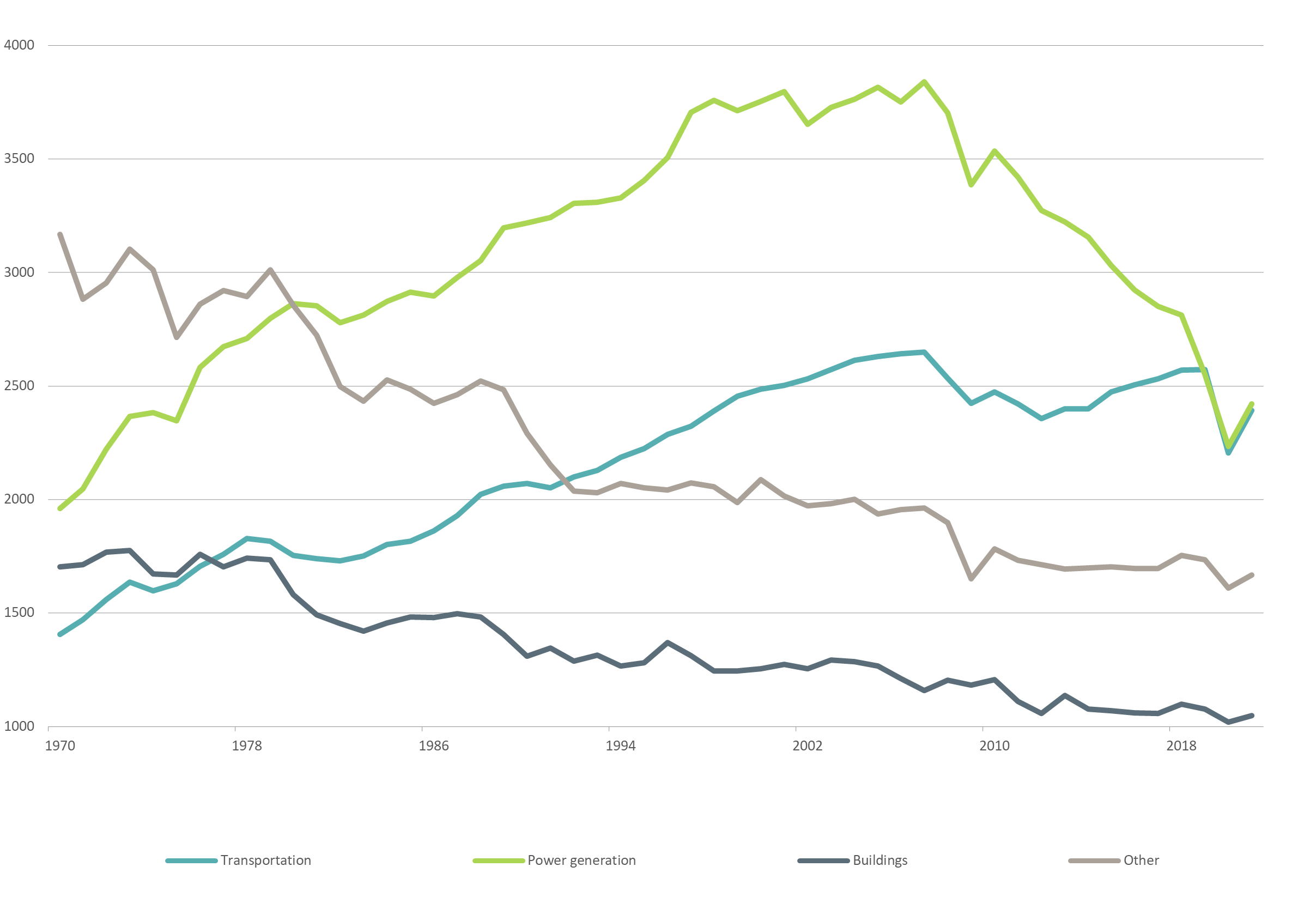

Carbon emissions by sector: Transportation still increasing

CO2 emissions in U.S. and EU in million tonnes

Source: Emissions Database for Global Atmospheric Research as of November 2023

Alas, as with any incumbents, the strength of utilities lies in sustaining technologies. Typically, this means catering to the needs of established, high-margin customers. The focus tends to be on incremental improvements to enhance existing products or services, rather than new niches.. Among utilities, this typically means adding capacity – and, quite often, intentionally or unintentionally hindering innovations that would disrupt their traditional business models.[3] The Innovator's Dilemma can help explain why countries that tried to push forward with their energy transition comparatively early tended to see incumbent utility companies resisting such necessary changes as “smart” metering.

By contrast, disruptive technologies[4] tend to be initially inferior for mainstream uses. Newcomers tend to focus on small, initially quite marginal niche segments neglected by incumbents. An excellent example concerns cars, even if it happens to be from 100 years ago. Well into the 1920s, sophisticated customers much preferred their nearly silent, easy-to-control and reliable electric cars. By comparison, early cars powered by internal combustion engines were seen as inconvenient, dirty and not very reliable.[5] Thanks to the electrification of car assembly lines and related product and process innovations, though, those high-emission gas guzzlers could soon be produced en masse, very cheaply.[6] Ever since, they have been the sustaining technology of legacy carmakers, which organized their organizations and processes around it.[7]

Electrification of car assembly lines eventually helped spell the end, until quite recently, for electric cars. This episode highlights how, as disrupting, enabling technologies improve, they tend to shake up many established business models in unpredictable ways. To take a more recent example, when the iPhone was introduced, it was by no means clear that it would create new competition for taxi companies.

Transportation is the only major sector globally where carbon emissions continue to rise (see chart), even in regions such as Europe that are otherwise advancing well on their journey towards net zero.[8] Governments and investors increasingly see it as an urgent priority. The distinction between sustaining versus disruptive technologies should make them cautious as to their ability to predict and pick potential winners. “Amid all the uncertainty surrounding disruptive technologies, managers can always count on one anchor: Experts’ forecasts will always be wrong."[9]